Chapter 5: Entrepreneurship: Starting and Managing Your Own Business

Learning Objectives

After reading this chapter, you should be able to answer these questions:

- Why do people become entrepreneurs, and what are the different types of entrepreneurs?

- What characteristics do successful entrepreneurs share?

- How do small businesses contribute to the Canadian economy?

- What are the first steps to take if you are starting your own business?

- Why does managing a small business present special challenges for the owner?

- What are the advantages and disadvantages of being an owner of a small business?

5.1 Entrepreneurship Today

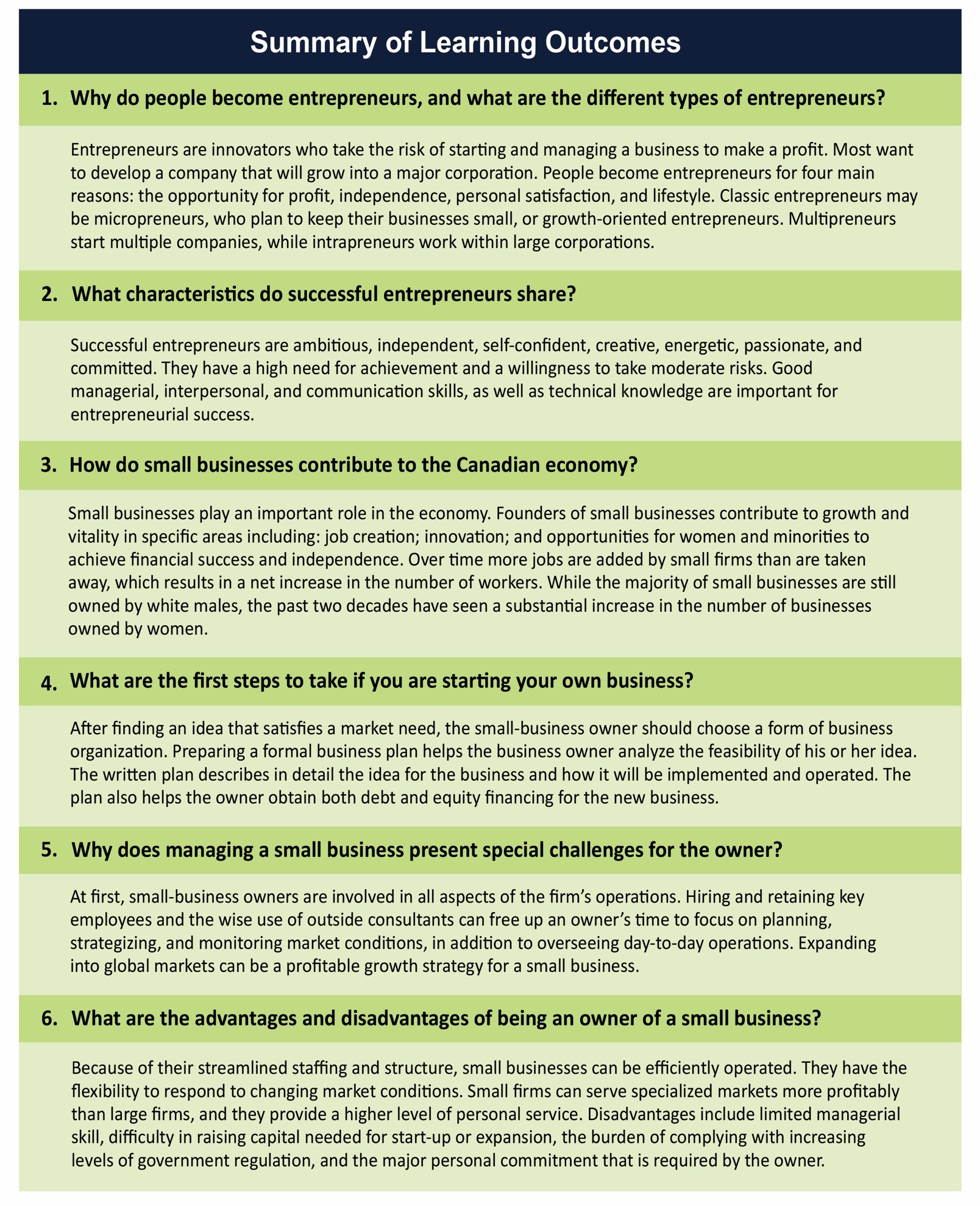

Why do people become entrepreneurs, and what are the different types of entrepreneurs?

Brothers Fernando and Santiago Aguerre exhibited entrepreneurial tendencies at an early age. At 8 and 9 years old respectively, they sold strawberries and radishes from a vacant lot near their parents’ home in Plata del Mar on the Atlantic coast of Argentina. At 11 and 12, they provided a surfboard repair service from their garage. As teenagers, Fer and Santi, as they call each other, opened Argentina’s first surf shop, which led to their most ambitious entrepreneurial venture of all.

The flat-footed brothers found that traipsing across hot sand in flip-flops was uncomfortable, so in 1984 they sank their $4,000 savings into manufacturing their own line of beach sandals. Now offering sandals and footwear for women, men, and children; clothing for men; Reef sandals have become the world’s hottest beach footwear, with a presence in nearly every surf shop in North America.[1]

The Aguerres, who currently live two blocks from each other in La Jolla, California, sold Reef to VF Corporation for more than $100 million in 2005. In selling Reef, “We’ve finally found our freedom,” Fernando says. “We traded money for time,” adds Santiago. Fernando remains active with surfing organizations, serving as president of the International Surfing Association, where he became known as “Ambassador of the Wave” for his efforts in getting all 90 worldwide members of the International Olympic Committee to unanimously vote in favour of including surfing in the 2020 Olympic Games.[2] He has also been named “Waterman of the Year” by the Surf Industry Manufacturers Association two times in 24 years.[3] Santi raises funds for his favorite not-for-profit, SurfAid. Both brothers are enjoying serving an industry that has served them so well.

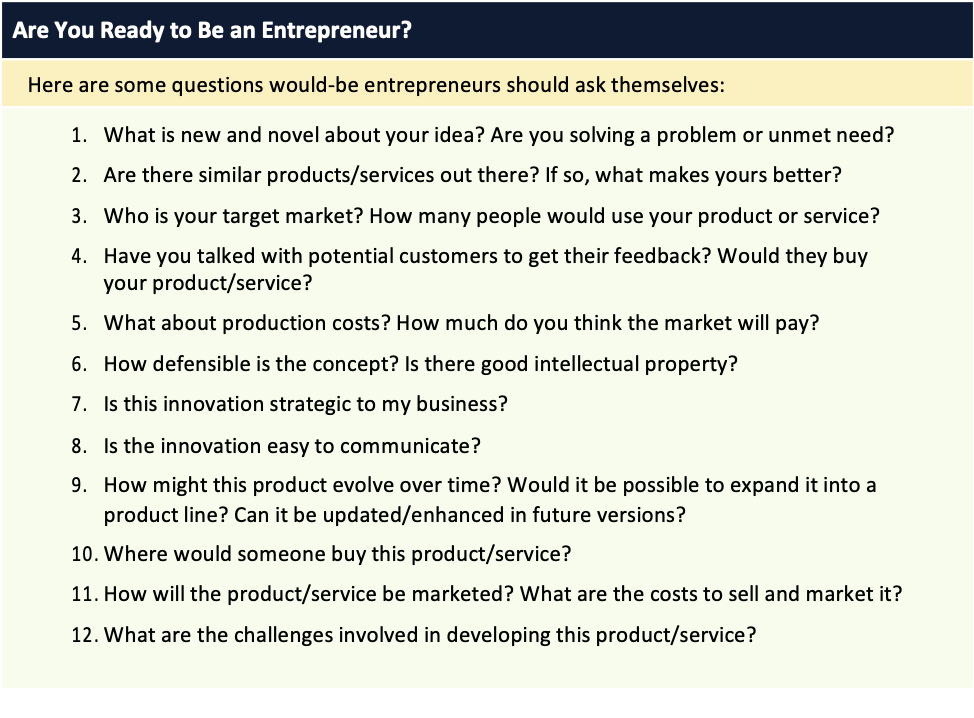

The world is blessed with a wealth of entrepreneurs such as the Aguerres who want to start a small business. According to research by the Small Business Administration, two-thirds of college students intend to be entrepreneurs at some point in their careers, aspiring to become the next Bill Gates or Jeff Bezos, founder of Amazon.com. But before you put out any money or expend energy and time, you’d be wise to check out Table 5.1 for some preliminary advice.

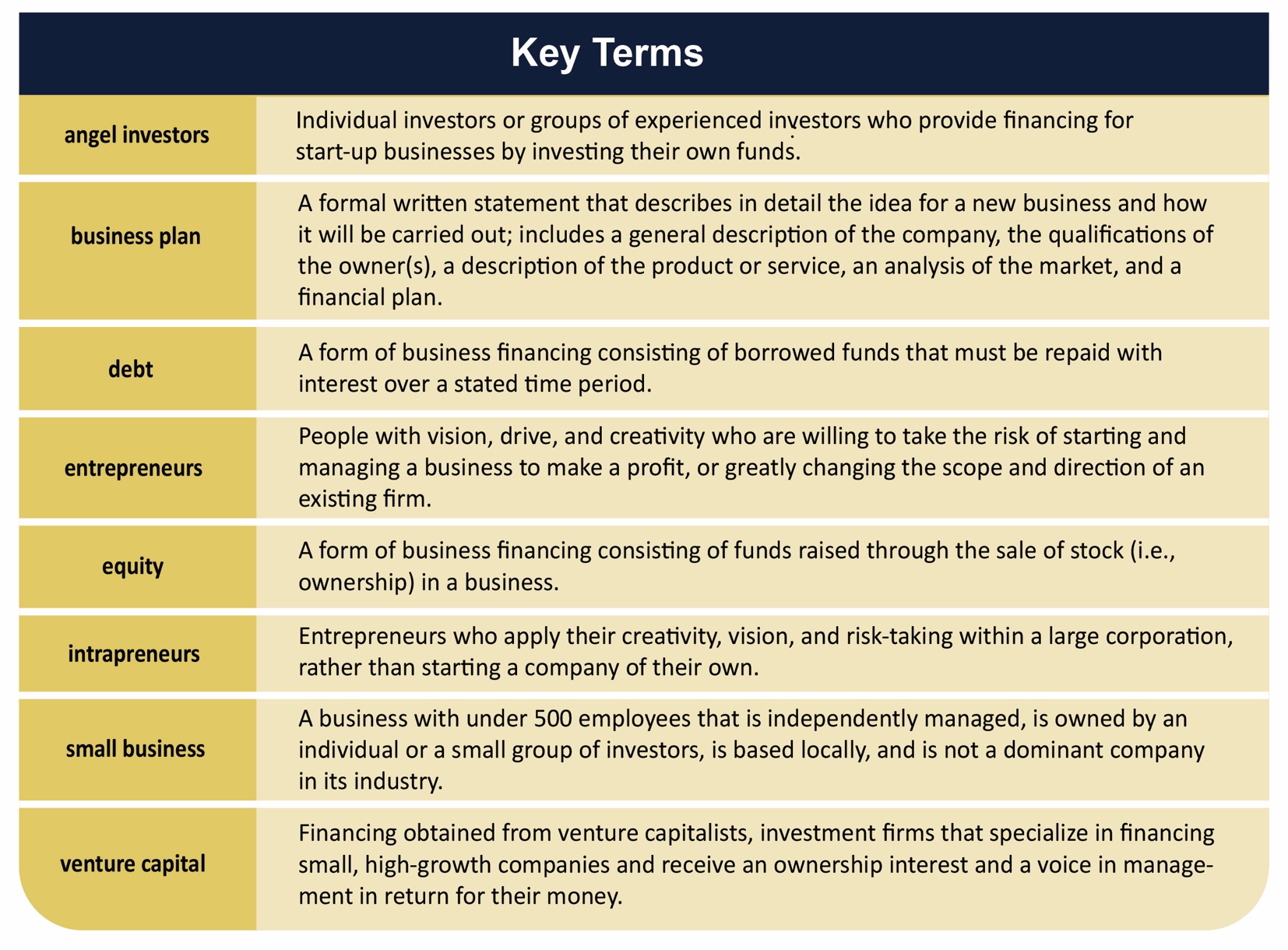

Why has entrepreneurship remained such a strong part of the foundation of the business system for so many years? Because today’s global economy rewards innovative, flexible companies that can respond quickly to changes in the business environment. Such companies are started by entrepreneurs, people with vision, drive, and creativity, who are willing to take the risk of starting and managing a business to make a profit.

Entrepreneur or Small-Business Owner?

The term entrepreneur is often used in a broad sense to include most small-business owners. The two groups share some of the same characteristics, and we’ll see that some of the reasons for becoming an entrepreneur or a small-business owner are very similar. But there is a difference between entrepreneurship and small- business management. Entrepreneurship involves taking a risk, either to create a new business or to greatly change the scope and direction of an existing one. Entrepreneurs typically are innovators who start companies to pursue their ideas for a new product or service. They are visionaries who spot trends.

Although entrepreneurs may be small-business owners, not all small-business owners are entrepreneurs. Small-business owners are managers or people with technical expertise who started a business or bought an existing business and made a conscious decision to stay small. For example, the proprietor of your local independent bookstore is a small-business owner. Jeff Bezos, founder of Amazon.com, also sells books. But Bezos is an entrepreneur: he developed a new model—web-based book retailing—that revolutionized the bookselling world and then moved on to change retailing in general. Entrepreneurs are less likely to accept the status quo, and they generally take a longer-term view than the small-business owner.

Types of Entrepreneurs

Entrepreneurs fall into several categories: classic entrepreneurs, multipreneurs, and intrapreneurs.

Classic Entrepreneurs

Classic entrepreneurs are risk-takers who start their own companies based on innovative ideas. Some classic entrepreneurs are micropreneurs who start small and plan to stay small. They often start businesses just for personal satisfaction and the lifestyle. Miho Inagi is a good example of a micropreneur. On a visit to New York with college friends in 1998, Inagi fell in love with the city’s bagels. “I just didn’t think anything like a bagel could taste so good,” she said. Her passion for bagels led the young office assistant to quit her job and pursue her dream of one day opening her own bagel shop in Tokyo. Although her parents tried to talk her out of it, and bagels were virtually unknown in Japan, nothing deterred her. Other trips to New York followed, including an unpaid six-month apprenticeship at Ess-a-Bagel, where Inagi took orders, cleared trays, and swept floors. On weekends, owner Florence Wilpon let her make dough.

In August 2004, using $20,000 of her own savings and a $30,000 loan from her parents, Inagi finally opened tiny Maruichi Bagel. The timing was fortuitous, as Japan was about to experience a bagel boom. After a slow start, a favourable review on a local bagel website brought customers flocking for what are considered the best bagels in Tokyo. Inagi earns only about $2,300 a month after expenses, the same amount she was making as a company employee. “Before I opened this store I had no goals,” she says, “but now I feel so satisfied.”[4]

In contrast, growth-oriented entrepreneurs want their business to grow into a major corporation. Most high- tech companies are formed by growth-oriented entrepreneurs. Jeff Bezos recognized that with Internet technology he could compete with large chains of traditional book retailers. Bezos’s goal was to build his company into a high-growth enterprise—and he chose a name that reflected his strategy: Amazon.com. Once his company succeeded in the book sector, Bezos applied his online retailing model to other product lines, from toys, house and garden items to tools, apparel, music, and services. In partnership with other retailers, Bezos is well on his way to making Amazon’s vision “to be Earth’s most customer-centric company; to build a place where people can come to find and discover anything they might want to buy online.”—a reality.[5]

Multipreneurs

Then there are multipreneurs, entrepreneurs who start a series of companies. They thrive on the challenge of building a business and watching it grow. In fact, over half of the chief executives at Inc. 500 companies say they would start another company if they sold their current one. Brothers Jeff and Rich Sloan are a good example of multipreneurs, having turned numerous improbable ideas into successful companies. Over the past 20-plus years, they have renovated houses, owned a horse breeding and marketing business, invented a device to prevent car batteries from dying, and so on. Their latest venture, a multimedia company called StartupNation, helps individuals realize their entrepreneurial dreams. And the brothers know what company they want to start next: yours.[6]

Intrapreneurs

Some entrepreneurs don’t own their own companies but apply their creativity, vision, and risk-taking within a large corporation. Called intrapreneurs, these employees enjoy the freedom to nurture their ideas and develop new products, while their employers provide regular salaries and financial backing. Intrapreneurs have a high degree of autonomy to run their own minicompanies within the larger enterprise. They share many of the same personality traits as classic entrepreneurs, but they take less personal risk. According to Gifford Pinchot, who coined the term intrapreneur in his book of the same name, large companies provide seed funds that finance in-house entrepreneurial efforts. These include Intel, IBM, Texas Instruments (a pioneering intrapreneurial company), Salesforce.com, and Xerox.

Why Become an Entrepreneur?

As the examples in this chapter show, entrepreneurs are found in all industries and have different motives for starting companies. The most common reason, cited by CEOs of the Inc. 500, the magazine’s annual list of fastest-growing private companies, is the challenge of building a business, followed by the desire to control their own destiny. Other reasons include financial independence and the frustration of working for someone else. Two important motives mentioned in other surveys are a feeling of personal satisfaction with their work and creating the lifestyle that they want. Do entrepreneurs feel that going into business for themselves was worth it? The answer is a resounding yes. Most say they would do it again.

5.2 Characteristics of Successful Entrepreneurs

What characteristics do successful entrepreneurs share?

Do you have what it takes to become an entrepreneur? Having a great concept is not enough. An entrepreneur must be able to develop and manage the company that implements his or her idea. Being an entrepreneur requires special drive, perseverance, passion, and a spirit of adventure, in addition to managerial and technical ability. Entrepreneurs are the company; they tend to work longer hours, take fewer vacations, and cannot leave problems at the office at the end of the day. They also share other common characteristics as described in the next section.

The Entrepreneurial Personality

Studies of the entrepreneurial personality find that entrepreneurs share certain key traits. Most entrepreneurs are:

- Ambitious: They are competitive and have a high need for achievement.

- Independent: They are individualists and self-starters who prefer to lead rather than follow.

- Self-confident: They understand the challenges of starting and operating a business and are decisive and confident in their ability to solve problems.

- Risk-takers: Although they are not averse to risk, most successful entrepreneurs favour business opportunities that carry a moderate degree of risk where they can better control the outcome over highly risky ventures where luck plays a large role.

- Visionary: Their ability to spot trends and act on them sets entrepreneurs apart from small-business owners and managers.

- Creative: To compete with larger firms, entrepreneurs need to have creative product designs, bold marketing strategies, and innovative solutions to managerial problems.

- Energetic: Starting and operating a business takes long hours. Even so, some entrepreneurs start their companies while still employed full-time elsewhere.

- Passionate: Entrepreneurs love their work, as Miho Inagi demonstrated by opening a bagel shop in Tokyo despite the odds against it being a success.

- Committed: Because they are so committed to their companies, entrepreneurs are willing to make personal sacrifices to achieve their goals.

Most entrepreneurs combine many of the above characteristics. Sarah Levy, 23, loved her job as a restaurant pastry chef but not the low pay, high stress, and long hours of a commercial kitchen. So she found a new one—in her parents’ home—and launched Sarah’s Pastries and Candies. Part-time staffers help her fill pastry and candy orders to the soothing sounds of music videos playing in the background. Conor McDonough started his own web design firm, OffThePathMedia.com, after becoming disillusioned with the rigid structure of his job. “There wasn’t enough room for my own expression,” he says. “Freelancing keeps me on my toes,” says busy graphic artist Ana Sanchez. “It forces me to do my best work because I know my next job depends on my performance.”[7]

Managerial Ability and Technical Knowledge

A person with all the characteristics of an entrepreneur might still lack the necessary business skills to run a successful company. Entrepreneurs need the technical knowledge to carry out their ideas and the managerial ability to organize a company, develop operating strategies, obtain financing, and supervise day-to-day activities. Jim Crane, who built Eagle Global Logistics from a start-up into a $250 million company, addressed a group at a meeting saying, “I have never run a $250 million company before so you guys are going to have to start running this business.”[8]

Good interpersonal and communication skills are important in dealing with employees, customers, and other business associates such as bankers, accountants, and attorneys. As we will discuss later in the chapter, entrepreneurs believe they can learn these much-needed skills. When Jim Steiner started his toner cartridge remanufacturing business, Quality Imaging Products, his initial investment was $400. He spent $200 on a consultant to teach him the business and $200 on materials to rebuild his first printer cartridges. He made sales calls from 8.00 a.m. to noon and made deliveries to customers from noon until 5:00 p.m. After a quick dinner, he moved to the garage, where he filled copier cartridges until midnight, when he collapsed into bed, sometimes covered with carbon soot. And this was not something he did for a couple of months until he got the business off the ground—this was his life for 18 months.[9] But entrepreneurs usually soon learn that they can’t do it all themselves. Often they choose to focus on what they do best and hire others to do the rest.

5.3 Small Business: Driving Canada’s Growth

How do small businesses contribute to the Canadian economy?

What Is a “Small Business”?

Small businesses are defined in many ways. Let’s start by looking at the criteria used by Industry Canada. In 2012 Industry Canada defined it as firms that have fewer than 100 employees. A small business is one that is independently owned and operated, exerting little influence in its industry.

Statistics for small businesses vary based on criteria such as new/start-up businesses, the number of employees, total revenue, length of time in business, nonemployees, businesses with employees, geographic location, and so on.

Although large corporations dominated the business scene for many decades, in recent years small businesses have once again come to the forefront. Downsizings that accompany economic downturns have caused many people to look toward smaller companies for employment, and they have plenty to choose from. Small businesses play an important role in the Canadian economy, representing about half of Canadian economic output, employing about half the private sector workforce, and giving individuals from all walks of life a chance to succeed.

Why are Small Businesses Important?

Small businesses are a force in Canada and other economies around the world. The millions of individuals who have started businesses have helped shape the business world as we know it today. Some small business founders like Henry Ford and Thomas Edison have even gained places in history. Others, including Bill Gates (Microsoft), Mike Lazaridis (Research in Motion), Steve Jobs (Apple Computer), and Larry Page and Sergey Brin (Google), have changed the way global business is done today.

Aside from contributions to our general economic well-being, founders of small businesses also contribute to growth and vitality in specific areas of economic and socio-economic development. In particular, small businesses do the following: create jobs. spark innovation, provide opportunities for many people, including women and minorities, to achieve financial success and independence. In addition, they complement the economic activity of large organizations by providing them with components, services, and distribution of their products. Let’s take a closer look at some of these contributions.

Job Creation

The majority of Canadian workers first entered the business world working for small businesses. Although the split between those working in small companies and those working in big companies is about even, small firms hire more frequently and fire more frequently than do big companies.15 Why is this true? At any given point in time, lots of small companies are started and some expand. These small companies need workers and so hiring takes place. But the survival and expansion rates for small firms is poor, and so, again at any given point in time, many small businesses close or contract and workers lose their jobs. Fortunately, over time more jobs are added by small firms than are taken away, which results in a net increase in the number of workers.

The size of the net increase in the number of workers for any given year depends on a number of factors, with the economy being at the top of the list. A strong economy encourages individuals to start small businesses and expand existing small companies, which adds to the workforce. A weak economy does just the opposite: discourages start-ups and expansions, which decreases the workforce through layoffs.

Opportunities for Women

Small business is the portal through which many people enter the economic mainstream. Business ownership allows individuals to achieve financial success, as well as pride in their accomplishments. While the majority of small businesses are still owned by white males, the past two decades have seen a substantial increase in the number of businesses owned by women.

Canada’s 2018 budget had continued investment in women entrepreneurs. On February 28, 2018, the Financial Post reported:

“By far, the largest net new impact on Canada’s entrepreneurial class is the $1.65 billion in new financing being made available to women business owners, to be delivered over three years through the Business Development Bank of Canada and Export Development Canada.”

5.4 Ready, Set, Start Your Own Business

What are the first steps to take if you are starting your own business?

You have decided that you’d like to go into business for yourself. What is the best way to go about it? Start from scratch? Buy an existing business? Or buy a franchise? About 75 percent of business start-ups involve brand-new organizations, with the remaining 25 percent representing purchased companies or franchises. Franchising may have been discussed elsewhere in your course, so we’ll cover the other two options in this section.

Getting Started

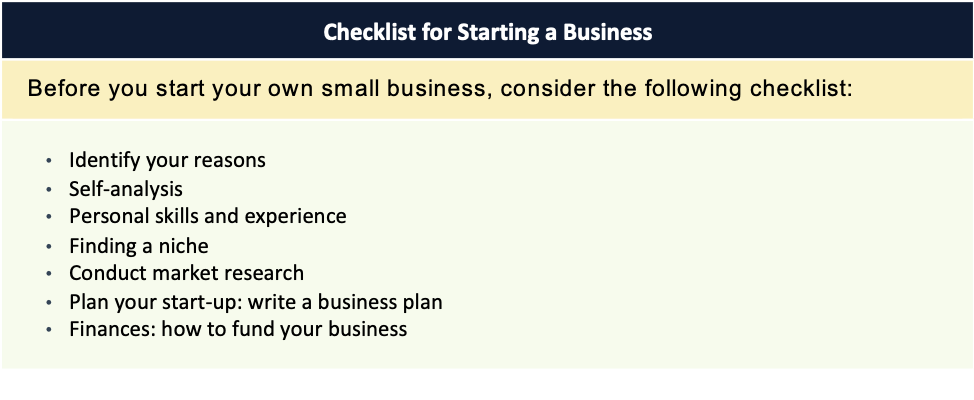

The first step in starting your own business is a self-assessment to determine whether you have the personal traits you need to succeed and, if so, what type of business would be best for you. Table 5.2 provides a checklist to consider before starting your business.

Finding the Idea

Entrepreneurs get ideas for their businesses from many sources. It is not surprising that about 80 percent of Inc. 500 executives got the idea for their company while working in the same or a related industry. Starting a firm in a field where you have experience improves your chances of success. Other sources of inspiration are personal experiences as a consumer; hobbies and personal interests; suggestions from customers, family, and friends; industry conferences; and college courses or other education.

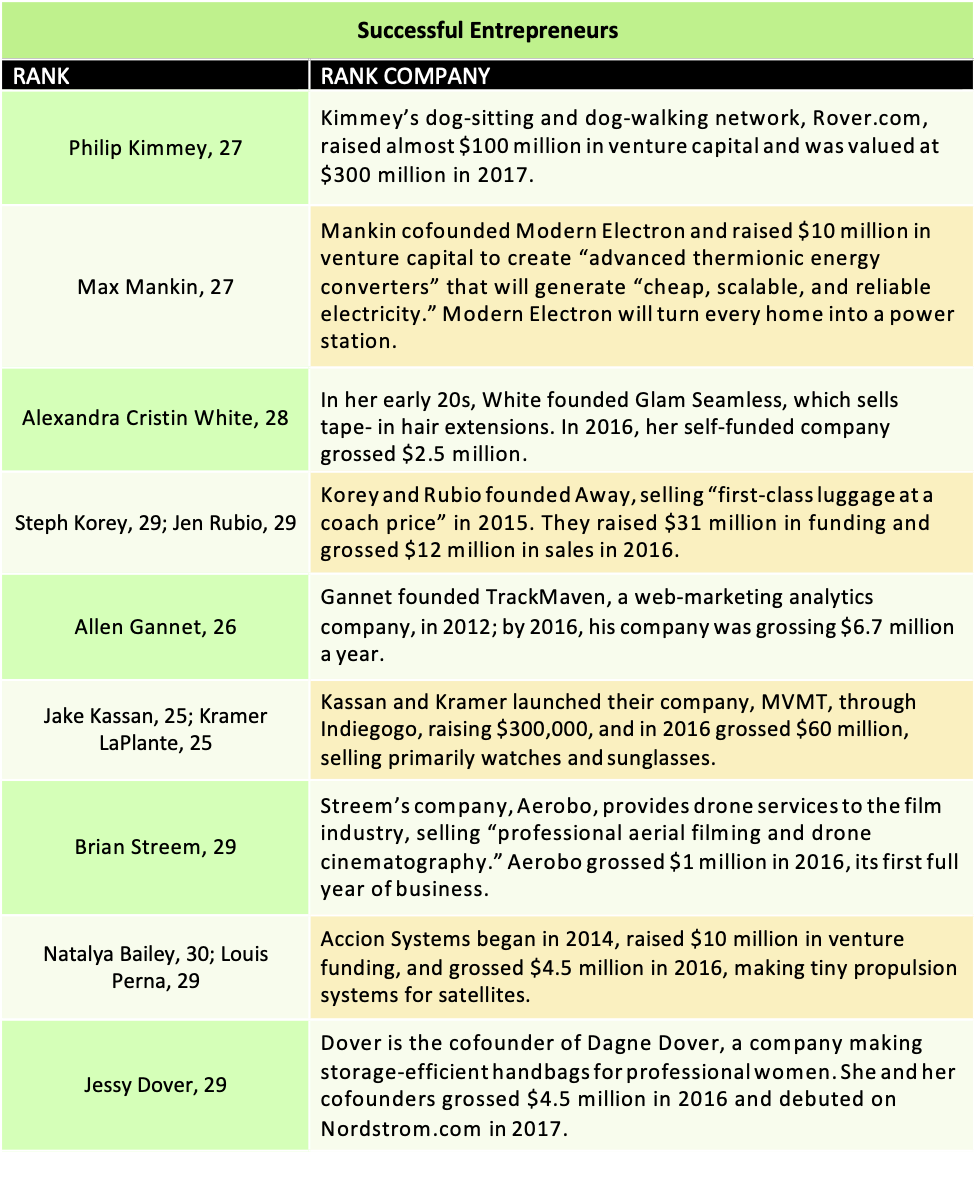

An excellent way to keep up with small-business trends is by reading entrepreneurship and small-business magazines and visiting their websites. With articles on everything from idea generation to selling a business, they provide an invaluable resource and profile some of the young entrepreneurs and their successful business ventures (Table 5.3).[10]

These dynamic individuals, who are already so successful in their 20s and 30s, came up with unique ideas and concepts and found the right niche for their businesses.

Interesting ideas are all around you. Many successful businesses get started because someone identifies a need and then finds a way to fill it. Do you have a problem that you need to solve? Or a product that doesn’t work as well as you’d like? Raising questions about the way things are done and seeing opportunity in adversity are great ways to generate ideas.

Choosing a Form of Business Organization

A key decision for a person starting a new business is whether it will be a sole proprietorship, partnership or corporation. As discussed earlier, each type of business organization has advantages and disadvantages. The choice depends on the type of business, number of employees, capital requirements, tax considerations, and the level of risk involved.

Developing the Business Plan

Once you have the basic concept for a product or service, you must develop a plan to create the business. This planning process, culminating in a sound business plan, is one of the most important steps in starting a business. It can help to attract appropriate loan financing, minimize the risks involved, and be a critical determinant in whether a firm succeeds or fails. Many people do not venture out on their own because they are overwhelmed with doubts and concerns. A comprehensive business plan lets you run various “what if” analyses and evaluate your business without any financial outlay or risk. You can also develop strategies to overcome problems well before starting the business.

Taking the time to develop a good business plan pays off. A venture that seems sound at the idea stage may not look so good on paper. A well-prepared, comprehensive, written business plan forces entrepreneurs to take an objective and critical look at their business venture and analyze their concept carefully; make decisions about marketing, sales, operations, production, staffing, budgeting and financing; and set goals that will help them manage and monitor its growth and performance.

The business plan also serves as the initial operating plan for the business. Writing a good business plan takes time. But many businesspeople neglect this critical planning tool in their eagerness to begin doing business, getting caught up in the day-to-day operations instead.

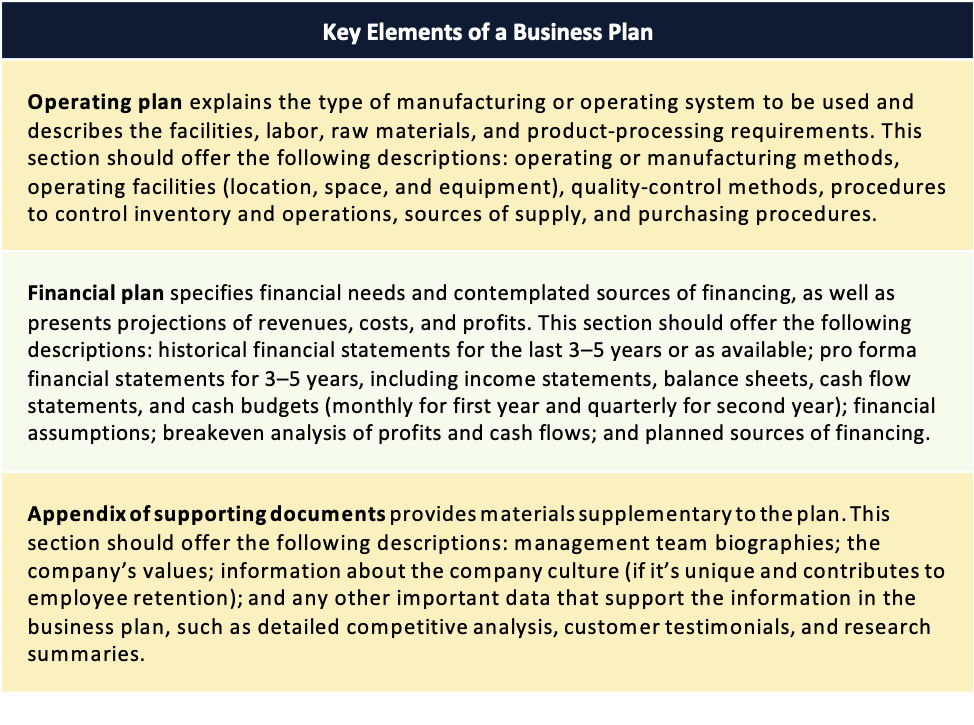

The key features of a business plan are a general description of the company, the qualifications of the owner(s), a description of the products or services, an analysis of the market (demand, customers, competition), sales and distribution channels, and a financial plan. The sections should work together to demonstrate why the business will be successful, while focusing on the uniqueness of the business and why it will attract customers. Table 5.4 describes the essential elements of a business plan.

A common use of a business plan is to persuade lenders and investors to finance the venture. The detailed information in the plan helps them assess whether to invest. Even though a business plan may take months to write, it must capture potential investors’ interest within minutes. For that reason, the basic business plan should be written with a particular reader in mind. Then you can fine-tune and tailor it to fit the investment goals of the investor(s) you plan to approach.

But don’t think you can set aside your business plan once you obtain financing and begin operating your company. Entrepreneurs who think their business plan is only for raising money make a big mistake. Business plans should be dynamic documents, reviewed and updated on a regular basis—monthly, quarterly, or annually, depending on how the business progresses and the particular industry changes.

Owners should adjust their sales and profit projections up or down as they analyze their markets and operating results. Reviewing your plan on a constant basis will help you identify strengths and weaknesses in your marketing and management strategies and help you evaluate possible opportunities for expansion considering both your original mission and goals, current market trends, and business results.

Financing the Business

Once the business plan is complete, the next step is to obtain financing to set up your company. The funding required depends on the type of business and the entrepreneur’s own investment. Businesses started by lifestyle entrepreneurs require less financing than growth-oriented businesses, and manufacturing and high- tech companies generally require a large initial investment.

Who provides start-up funding for small companies? Like Miho Inagi and her Tokyo bagel shop, 94 percent of business owners raise start-up funds from personal accounts, family, and friends. Personal assets and money from family and friends are important for new firms, whereas funding from financial institutions may become more important as companies grow. Three-quarters of Inc. 500 companies have been funded on $100,000 or less.[11]

The two forms of business financing are debt, borrowed funds that must be repaid with interest over a stated time period, and equity, funds raised through the sale of stock (i.e., ownership) in the business. Those who provide equity funds get a share of the business’s profits. Because lenders usually limit debt financing to no more than a quarter to a third of the firm’s total needs, equity financing often amounts to about 65 to 75 percent of total start-up financing.

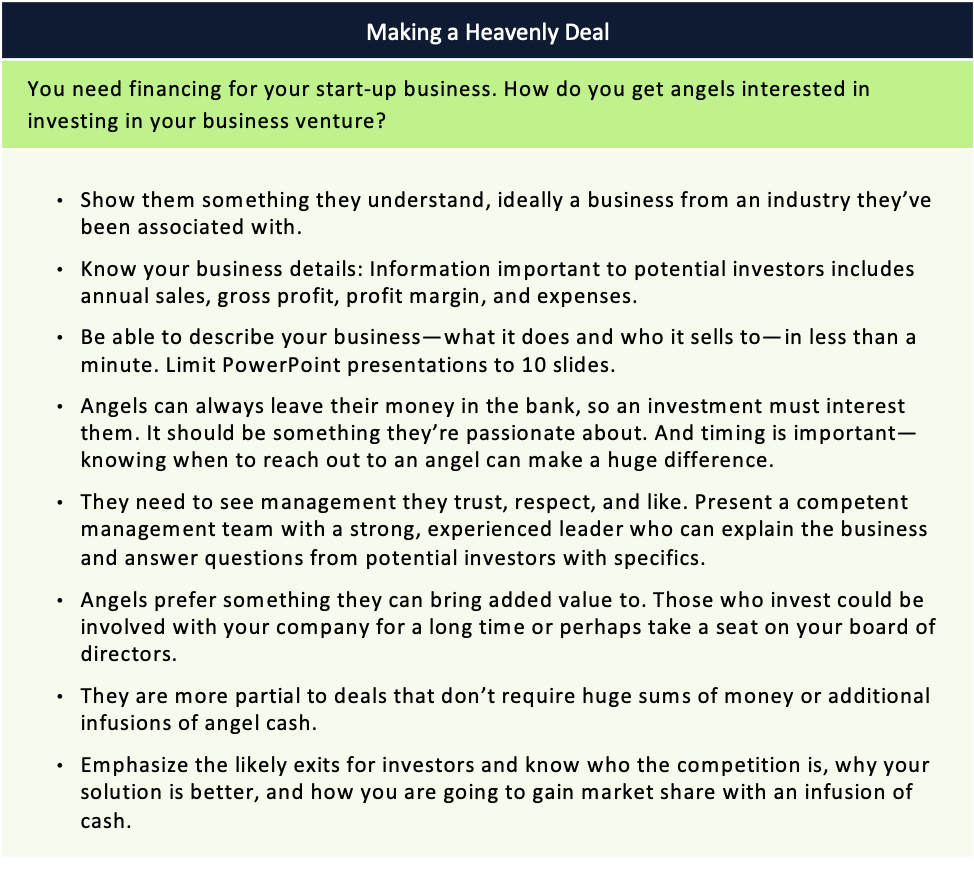

One way to finance a start-up company is bootstrapping, which is basically funding the operation with your own resources. If the resources needed are not available to an individual, there are other options. Two sources of equity financing for young companies are angel investors and venture-capital firms. Angel investors are individual investors or groups of experienced investors who provide financing for start-up businesses by investing their own money, often referred to as “seed capital.” This gives the investors more flexibility on what they can and will invest in, but because it is their own money, angels are careful. Angel investors often invest early in a company’s development, and they want to see an idea they understand and can have confidence in. Table 5.5 offers some guidelines on how to attract angel financing.

Venture capital is financing obtained from venture capitalists, investment firms that specialize in financing small, high-growth companies. They typically invest at a later stage than angel investors. It is most often used by small and growing firms that aren’t big enough to sell securities to the public. This type of financing is especially popular among high-tech companies that need large sums of money.

Venture capitalists invest in new businesses in return for part of the ownership, sometimes as much as 60 percent. They look for new businesses with high growth potential, and they expect a high investment return within 5 to 10 years. By getting in on the ground floor, venture capitalists buy stock at a very low price. They earn profits by selling the stock at a much higher price when the company goes public. Venture capitalists generally get a voice in management through seats on the board of directors. Getting venture capital is difficult, even though there are hundreds of private venture-capital firms. Most venture capitalists finance only about 1 to 5 percent of the companies that apply. Venture-capital investors, many of whom experienced losses during recent years from their investments, are currently less willing to take risks on very early-stage companies with unproven business concepts or technology. As a result, other sources of venture capital, including private foundations, and wealthy individuals (called angel investors), are helping start-up firms find equity capital. These private investors are motivated by the potential to earn a high return on their investment.

Buying a Small Business

Another route to small-business ownership is buying an existing business. Although this approach is less risky, many of the same steps for starting a business from scratch apply to buying an existing company. It still requires careful and thorough analysis. The potential buyer must answer several important questions: Why is the owner selling? Does he or she want to retire or move on to a new challenge, or are there problems with the business? Is the business operating at a profit? If not, can this be corrected? On what basis has the owner valued the company, and is it a fair price? What are the owner’s plans after selling the company? Will he or she be available to provide assistance through the change of ownership of the business? And depending on the type of business it is, will customers be more loyal to the owner than to the product or service being offered? Customers could leave the firm if the current owner decides to open a similar business. To protect against this, many purchasers include a noncompete clause in the contract of sale, which generally means that the owner of the company being sold may not be allowed to compete in the same industry of the acquired business for a specific amount of time.

Risky Business

You should prepare a business plan that thoroughly analyzes all aspects of the business. Get answers to all your questions, and determine, via the business plan, whether the business is a sound one. Then you must negotiate the price and other terms of purchase and obtain appropriate financing. This can be a complicated process and may require the use of a consultant or business broker.

Running your own business may not be as easy as it sounds. Despite the many advantages of being your own boss, the risks are great as well. Over a period of five years, nearly 50% percent of small businesses fail according to the Kauffman Foundation.[12]

Businesses close for many reasons—and not all are failures. Some businesses that close are financially successful and close for nonfinancial reasons. But the causes of business failure can be interrelated. For example, low sales and high expenses are often directly related to poor management. Some common causes of business closure are:

- Economic factors—business downturns and high interest rates

- Financial causes—inadequate capital, low cash balances, and high expenses

- Lack of experience—inadequate business knowledge, management experience, and technical expertise

- Personal reasons—the owners may decide to sell the business or move on to other opportunities

Inadequate early planning is often at the core of later business problems. As described earlier, a thorough feasibility analysis, from market assessment to financing, is critical to business success. Yet even with the best plans, business conditions change, and unexpected challenges arise. An entrepreneur may start a company based on a terrific new product only to find that a larger firm with more marketing, financing, and distribution clout introduces a similar item.

The stress of managing a business can also take its toll. The business can consume your whole life. Owners may find themselves in over their heads and unable to cope with the pressures of business operations, from the long hours to being the main decision maker. Even successful businesses must deal with ongoing challenges. Growing too quickly can cause as many problems as sluggish sales. Growth can strain a company’s finances when additional capital is required to fund expanding operations, from hiring additional staff to purchasing more raw material or equipment. Successful business owners must respond quickly and develop plans to manage its growth.

So, how do you know when it is time to quit? “Never give up” may be a good motivational catchphrase, but it is not always good advice for a small-business owner. Yet, some small-business owners keep going no matter what the cost. For example, Ian White’s company was trying to market a new kind of city map. White maxed out 11 credit cards and ran up more than $100,000 in debt after starting his company. He ultimately declared personal bankruptcy and was forced to find a job so that he could pay his bills. Maria Martz didn’t realize her small business would become a casualty until she saw her tax return showing her company’s losses in black and white—for the second year in a row. It convinced her that enough was enough and she gave up her gift- basket business to become a full-time homemaker. But once the decision is made, it may be tough to stick to. “I got calls from people asking how come I wasn’t in business anymore. It was tempting to say I’d make their basket, but I had to tell myself it is finished now.”[13]

5.5 Managing a Small Business

Why does managing a small business present special challenges for the owner?

Managing a small business is quite a challenge. Whether you start a business from scratch or buy an existing one, you must be able to keep it going. The small-business owner must be ready to solve problems as they arise and move quickly if market conditions change.CH

A sound business plan is key to keeping the small-business owner in touch with all areas of his or her business. Hiring, training, and managing employees is another important responsibility because the owner’s role may change over time. As the company grows, others will make many of the day-to-day decisions while the owner focuses on managing employees and planning for the firm’s long-term success. The owner must constantly evaluate company performance and policies, consider changing market and economic conditions, and develop new policies as required. He or she must also nurture a continual flow of ideas to keep the business growing. The types of employees needed may change too as the firm grows. For instance, a larger firm may need more managerial talent and technical expertise.

Using Outside Consultants

One way to ease the burden of managing a business is to hire outside consultants. Nearly all small businesses need a good certified public accountant (CPA) who can help with financial record keeping, decision-making, and tax planning. An accountant who works closely with the owner to help the business grow is a valuable asset. An attorney who knows about small-business law can provide legal advice and draw up essential contracts and documents. Consultants in areas such as marketing, employee benefits, and insurance can be used on an as-needed basis. Outside directors with business experience are another way for small companies to get advice. Resources such as these free the small-business owner to concentrate on medium- and long- range planning and day-to-day operations.

Some aspects of business can be outsourced or contracted out to specialists. Among the more common departments that use outsourcing are information technology, marketing, customer service, order fulfillment, payroll, and human resources. Hiring an outside company—in many cases another small business—can save money because the purchasing firm buys just the services it needs and makes no investment in expensive technology. Management should review outsourced functions as the business grows because at some point it may be more cost-effective to bring them in-house.

Hiring and Retaining Employees

It is important to identify all the costs involved in hiring an employee to make sure your business can afford it. Recruiting, help-wanted ads, extra space, and taxes will easily add about 10–15 percent to their salary, and employee benefits will add even more. Hiring an employee may also mean more work for you in terms of training and management. It’s a catch-22: to grow you need to hire more people but making the shift from solo worker to boss can be stressful.

Attracting good employees is more difficult for a small firm, which may not be able to match the higher salaries, better benefits, and advancement potential offered by larger firms. Small companies need to be creative to attract the right employees and convince applicants to join their firm. Once they hire an employee, small-business owners must make employee satisfaction a top priority in order to retain good people. A company culture that nurtures a comfortable environment for workers, flexible hours, employee benefit programs, opportunities to help make decisions, and a share in profits and ownership are some ways to do this.

Duane Ruh figured out how to build a $1.2 million business in a town with just 650 residents. It’s all about treating employees right. The log birdhouse and bird feeder manufacturer, Little Log Co., located in Sargent, Nebraska, boasts employee-friendly policies you read about but rarely see put into practice. Ruh offers his employees a flexible schedule that gives them plenty of time for their personal lives. During a slow period, last summer, Ruh cut back on hours rather than lay anyone off. There just aren’t that many jobs in that part of Nebraska that his employees could go to, so when he received a buyout offer that would have closed his facility but kept him in place with an enviable salary, he turned it down. Ruh also encourages his employees to pursue side or summer jobs if they need to make extra money, assuring them that their Little Log jobs are safe.[14]

Going Global with Exporting

More and more small businesses are discovering the benefits of looking beyond Canada for market opportunities. The global marketplace represents a huge opportunity for Canadian businesses, both large and small. Small businesses’ decision to export is driven by many factors, one of which is the desire for increased sales and higher profits. Canadian goods are less expensive for overseas buyers when the value of the Canadian dollar declines against foreign currencies, and this creates opportunities for Canadian companies to sell globally. In addition, economic conditions such as a domestic recession, foreign competition within Canada, or new markets opening up in foreign countries may also encourage Canadian companies to export.

Like any major business decision, exporting requires careful planning. Small businesses may hire international-trade consultants or distributors to get started selling overseas. These specialists have the time, knowledge, and resources that most small businesses lack. Export trading companies (ETCs) buy goods at a discount from small businesses and resell them abroad. Export management companies (EMCs) act on a company’s behalf. For fees of 5–15 percent of gross sales and multiyear contracts, they handle all aspects of exporting, including finding customers, billing, shipping, and helping the company comply with foreign regulations.

5.6 Small Business, Large Impact

What are the advantages and disadvantages of being an owner of a small business?

Advantages of Small Business Ownership:

- Independence: Large corporations no longer represent job security or offer the fast- track career opportunities they once did. Mid-career employees leave the corporate world—either voluntarily or because of downsizing—in search of the new opportunities that self-employment provides. Many new college and business school graduates shun the corporate world altogether to start their own companies or look for work in smaller firms.

- Personal satisfaction from work: Many small-business owners cite this as one of the primary reasons for starting their companies. They love what they do.

- Best route to success: Business ownership provides greater advancement opportunities for women and minorities. It also offers small-business owners the potential for profit.

- Rapidly changing technology: Technology advances and decreased costs provide individuals and small companies with the power to compete in industries that were formerly closed to them.

- Major corporate restructuring and downsizing: This forces many employees to look for other jobs or careers. It may also provide the opportunity to buy a business unit that a company no longer wants.

- Outsourcing: As a result of downsizing, corporations may contract with outside firms for services they used to provide in-house. Outsourcing creates opportunities for smaller companies that offer these specialized goods and services.

- Small businesses are resilient: They can respond fairly quickly to changing economic conditions by refocusing their operations.

Disadvantages of Small Business Ownership:

- Financial risk: The financial resources needed to start and grow a business can be extensive. You may need to commit most of your savings or even go into debt to get started. If things don’t go well, you may face substantial financial loss. In addition, there’s no guaranteed income. There might be times, especially in the first few years, when the business isn’t generating enough cash for you to live on.

- Stress: As a business owner, you are the business. There’re many things to worry about—competition, employees, bills, equipment breakdowns, etc. As the owner, you’re also responsible for the well-being of your employees.

- Time commitment: People often start businesses so that they’ll have more time to spend with their families. Unfortunately, running a business is extremely time-consuming. In theory, you have the freedom to take time off, but in reality, you may not be able to get away. In fact, you’ll probably have less free time than you’d have working for someone else. For many entrepreneurs and small business owners, a forty-hour workweek is a myth. Vacations will be difficult to take and will often be interrupted. In recent years, the difficulty of getting away from the job has been compounded by cell phones, iPhones, Internet-connected laptops and iPads, and many small business owners have come to regret that they’re always reachable.

- Undesirable duties: When you start up, you’ll undoubtedly be responsible for either doing or overseeing just about everything that needs to be done. You can get bogged down in detail work that you don’t enjoy. As a business owner, you’ll probably have to perform some unpleasant tasks, like firing people.

- Limitations: On the other hand, being small is not always an asset. The founders may have limited managerial skills or encounter difficulties obtaining adequate financing, potential obstacles to growing a company. Complying with federal regulations is also more expensive for small firms. Those with fewer than 20 employees spend about twice as much per employee on compliance than do larger firms. In addition, starting and managing a small business requires a major commitment by the owner. Long hours, the need for owners to do much of the work themselves, and the stress of being personally responsible for the success of the business can take a toll.

Key Terms

Summary of Learning Outcomes

- Shannon McMahon, “Stepping into a Fortune,” San Diego Union-Tribune, April 5, 2005, p. C4. ↵

- Dashel Pierson, “10 Things You Should Know about Surfing in the Olympics,” Surfline, http://www.surfline.com, August 5, 2016 ↵

- Steve Chapple, “Reef Brand’s Co-founder Eyes the Horizon,” San Diego Union Tribune, https://www.sandiegouniontribune.com, December 13, 2013. ↵

- Andrew Morse, “An Entrepreneur Finds Tokyo Shares Her Passion for Bagels,” The Wall Street Journal, October 18, 2005, p. B1. ↵

- Barbara Farfan, “Amazon.com’s Mission Statement”, The Balance. April 15, 2018, https://www.thebalance.com/amazon-mission-statement-4068548. ↵

- “About StartupNation,” https://startupnation.com, accessed February 1, 2018; Jim Morrison, “Entrepreneurs,” American Way Magazine, October 15, 2005, p. 94. ↵

- Martha Irvine, “More 20-Somethings Are Blazing Own Paths in Business,” San Diego UnionTribune, November 22, 2004, p. C6. ↵

- Keith McFarland, “What Makes Them Tick,” Inc. 500, October 19, 2005, http://www.inc.com. ↵

- Ibid. ↵

- Adapted from “They’ve Founded Million Dollar Companies and They’re not Even 30,”https://www.inc.com/30-under-30. ↵

- McFarland, “What Makes Them Tick.” ↵

- “The Kauffman Index,” http://www.kauffman.org, accessed February 2, 2018. ↵

- Andrew Blackman, “Know When to Give Up,” The Wall Street Journal, May 9, 2005, p. R9. ↵

- Michelle Prather, “Talk of the Town,” Entrepreneur Magazine, February 2003, http://www.entrepreneur.com. ↵

A business with under 500 employees that is independently managed, is owned by an individual or a small group of investors, is based locally, and is not a dominant company in its industry.

People who combine inputs of natural resources, labour, and capital to produce goods or services with the intention of making a profit or accomplishing a not-for-profit goal.

risk-takers who start their own business based on innovative ideas.

Entrepreneurs who start small and plan to stay small.

Entrepreneurs who want their business operation to grow into a major corporation.

Entrepreneurs who apply their creativity, vision and risk-taking within a large corporation, rather than starting their own company.

A formal written statement that describes in detail the idea for a new business and how it will be carried outs; includes a general description of the company, the qualifications of the owner(s), a description of the product or service, an analysis of the market, and a financial plan.

A form of business financing consisting of borrowed funds that must be repaid with interest over a stated period.

A form of business financing consisting of funds raised through the sale of stock (i.e. ownership) in a business.

Individual investors or groups of experienced investors who provide financing for start-up businesses by investing their own funds.

Financing obtained from venture capitalists, investment firms that specialize in financing small, high growth oriented companies and receive an ownership interest and a voice in management in return for their money.